Whenever, we hear the word ‘Retirement’, our provoking thought that, there is enough time ahead and this way months and years pass on. We have done everything for our children and family, and completed all the responsibilities of life, but have terribly forgotten about retirement planning. All life, we have earned and spent it on others, but now when time would come, we would not have enough money to survive a fulfilling life for rainy days.

It will not matter if you have planned for your retirement years or not it because you don’t set the goal of retirement. It’s already SET. You are approaching it each year, each month, each day, and each hour and each second, very slowly. Now you just have to get prepare yourself. For every year and every month you do not save for future, you are short for that particular retirement year. Your time left for retirement decreases, but you still have to save more and more with each passing year.

Two Engines of Growth

By passing of time, for any retirement corpus has required two engines of growth: the contributions made by you, and the rate of return generated by the portfolio. But which has the greater impact?

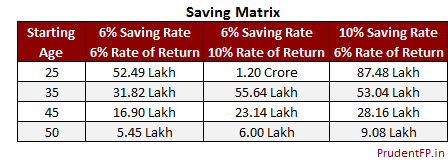

To get know the better understanding, get ready for playing magical game with numbers. So, we draw the Saving Matrix which will show you various astounding generated corpus at age 60 based on four different starting ages of an investor.

For the simplicity of calculations, we assume Rs5 lakh per annum starting salary at age 25 with 3% annual increase in pay. A detailed analysis is designed to isolate the impact of changing the savings rate versus changes in the rate of portfolio return revealed that the answer would depend greatly on a person’s age.

In the above saving matrix, the baseline figures in the first column assume an annual savings rate of 6% of income and an annualized portfolio return of 6%. The other two columns show how the results would vary if the savings rate were to jump to 10% or if the portfolio return were to increase to 10%, while holding the other variable constant.

For an investor who begins contributing to an investment portfolio at 25, the baseline terminal value at 60 is Rs52.49 lakh. If the annual portfolio returns increases to 10% and the savings rate stays at 6%, the portfolio value at 60 soars to nearly Rs1.20 crore. On the other hand, if the savings rate increases to 10% a year and the portfolio return stays at 6%, the ending portfolio value at 60 is Rs87.48 lakh.

Of course, here, it must be advisable that the best of all worlds for a 25-year-old person is to save 10% of income each year and have a portfolio return of 10%. No question about that – the ending portfolio value would be a sweet Rs2.00 crore.

But clearly, for a young person, the portfolio rate of return has more impact on the ultimate account value than the annual savings rate.

Next, consider an investor just getting started at 35 years old. Assuming a 6% savings rate and a 6% annualized portfolio return, the baseline portfolio value at 60 is Rs31.82 lakh (assuming annual salary of Rs6.72 lakh at age 35 with 3% annual increase in pay). If the portfolio’s annual rate of return increases to 10% while the savings rate is constant at 6%, the ending account value at 60 is Rs55.64 lakh, compared with Rs53.04 lakh if the savings rate is increased to 10% while holding the portfolio return at 6% annually. Once again, for a younger person, an increase in the portfolio return provides greater impact than the same increase in the savings rate.

Saving Rate overrides Portfolio Return

But at age 45, the math gets interesting. A person who starts investing at that point benefits more from increasing his savings rate to 10% than from attempting to increase his portfolio return to 10%.

This may be counterintuitive; the conventional wisdom might suggest that if a person is late to the retirement game, he needs to make up for lost time by trying to build a portfolio that can crank out returns of 10% to 12% a year. This research suggests otherwise. In fact, the older investor needs to save more each year rather than build an overly aggressive, high-risk/high-return equity portfolio.

Think of it this way: If the time frame of a person is reduced to 20 years from 35 years, the beneficial impact of compounding is drastically reduced. Since the dramatic compounding-based growth in a portfolio really starts to pick up steam after 20 to 25 years, within shorter time frames, a portfolio benefits more from direct contributions.

For an investor who starts saving at age 50, raising the savings rate to 10% of income produces an ending account value that is nearly Rs3.08 lakh higher than if the portfolio return is raised to 10%. Clearly, this is an investor who is very late to the game – Such investors need to do all they can to prepare for retirement. These results clearly indicate that saving as much of their income as they can has a greater impact than cranking up the portfolio risk to try to generate higher returns.

Contributions are a variable that is more in the control of the investor, while portfolio performance, particularly in the short run, is far less controllable. As a result, investors who rely upon portfolio performance to do their heavy lifting will usually fall into the trap of having too much equity exposure and, therefore, too much risk.

Particularly for persons who are in or near retirement, the performance of an investment portfolio should accomplish two primary goals: preserve and protect principal and provide a modest rate of return.

Power of both Engines

Consider a simplistic example that illustrates the importance of not deferring saving. Once again, same young person at 25-year-old begins his career earning Rs5 lakh per year, and that his salary increases 3% annually over the next 35 years. If he invests 10% of his income each year in a provident fund – with, say, his own 6% savings and a 4% match from his employer – he will have a nominal balance of Rs31.64 lakh accumulated by the time he’s 60 if the portfolio earns a rate of return of 0%. That is, he will have nearly one-third of Rs1 crore entirely as a result of his own contributions, the first engine of growth.

Now, let’s consider the second engine of growth, portfolio performance. If his PF account averages an annualized return of 6% per year, his account value when he’s 60 will be Rs87.48 lakh (of which Rs31.64 lakh will be his contributions). Clearly, the “return” of the portfolio is a significant part of the ending account value, along with his contributions.

Optimum Contribution

Now assume the 25-year-old invests only 2% of his salary each year until he retires at 60. Assuming a 0% return in his retirement portfolio, he would have an account balance of Rs6.33 lakh. And with a 6% average annualized return over 35 years, his balance would be only Rs17.50 lakh.

To achieve an ending balance of Rs87.48 lakh by the time he’s 60 while maintaining his low 2% contribution rate, his retirement portfolio would need to generate an average annualized return of 13.4%. In other words, his inadequate contributions force the portfolio to (try to) do the heavy lifting in equity. Can a portfolio reasonably be expected to produce an average annualized return of 13.4% over a 35-year period?

This type of hypothetical analysis can go on forever, but the reality is glaring: A 2% savings rate is not adequate preparation for retirement. For that matter, not even a 4% savings rate is adequate.

Conclusion

The most important step that can be taken to be better prepared financially for retirement; you would be to increase the annual savings rate to at least 6% of income. A rate of 10% would be that much better. For investors older than 45, this is even more vitally important.

If you are at young stage and willing to take more risk, there is a distinct payoff in the long run – and you have the crucial benefit of time on your side. But for older one, taking on more risk exposes him to losses that he has neither the time to recoup nor the emotional stamina to endure.