So in practice the whole scheme becomes like a recurring deposit where you deposit some money each month. The bonus instalment deposited by jeweller makes sure you get a return around 8-10% on the overall instalment.

Mandatory to buy Gold jewellery

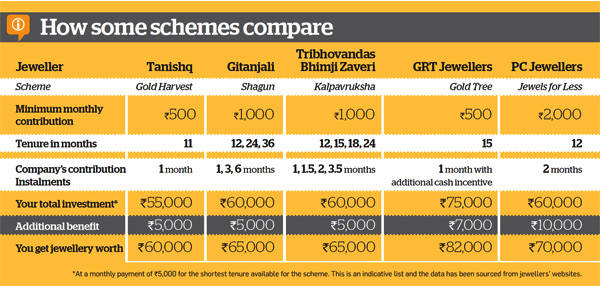

Like recurring deposits, you can’t convert the money accumulated in gold kitty saving schemes into cash. The gold saving schemes make it mandatory that you have to buy gold jewellery and only gold jewellery, not even gold bars or coins. So in case you need money for some other purpose, you can’t use it. But you will say that it’s fine, because at times you also are offered “Zero Making Charges” under these schemes, but you miss reading the terms and conditions which says that it’s only on selected designs and models. What if you do not want to buy those designs? In that case you have to pay the making charges which are applicable and what happens if the design and model which you like have much higher price than you have accumulated? In that case you have to shell out more money. The making charges which you will pay will cancel out the 8-10% returns which you make on the whole scheme.

Mutual Fund Gold Saving Schemes versus Jeweller Gold Saving Scheme

- Almost every jeweller forces you to buy gold jewellery and does not give you cash in return. Hence, you are forced to pay making charges for the jewellery and end up paying extra cash or buying less gold. In contrast, a gold savings scheme by mutual fund returns cash at the end of the tenure and thus you are saved from paying extra in the form of making charges.

- The gold savings scheme by jewellers does not have SEBI approval and thus there is no monitoring of the cash you pay. These jewellers may well be using your funds for meeting their working capital requirements or business needs since there is no regulator who keeps a check on their books. So, if tomorrow, suddenly gold price crashes and all investors stop their instalments and demand for gold, and then it may well turn out that some of the jewellers would be unable to honour their commitment. On the other hand, gold savings schemes of mutual funds are governed by SEBI. Their books are mandatorily checked and all the funds/investments are backed by physical gold.

- Very few jewellers offer 24 carat gold; almost every jeweller offers only 22 carat gold. Since you have no option but to purchase gold, you end up buying gold which is not 100% pure. In a mutual fund gold savings scheme, your funds are backed by 24 carat pure gold.

- In such schemes, your gold purchase attracts wealth tax and also capital gain tax, if you sell within 3 years. In the mutual fund’s scheme, there is no wealth tax. Further, Gold ETFs are eligible for the long-term capital gains after just one year, unlike physical gold, which is eligible for long-term capital gains after three years.

Which scheme you should choose?

So given these fine points, gold jewellery schemes aim to give you gold/Jewellery whereas mutual fund gold savings schemes/Gold ETFs aim to give you cash. So, if you want to buy jewellery in the near future, say 1 year, then go for gold savings schemes of the jewellery companies, but if you want to buy gold for the purpose of investment or if your gold usage is at a later date, when you have a marriage or function due in several years, then opt for gold savings fund/Gold ETFs. A caveat for those opting for the jewellery schemes unless you have a very trusted and reliable jeweller and ready to buy back from you, do not opt for these. Buy Gold ETFs, sell the units when you want gold and from the money you get, go buy gold!

What is worth considering?

In our opinion, gold continues to be a non-productive asset and over long periods of time, returns from gold seldom beat returns from productive assets classes like equities, unless you are an active investor who spends a lot of time rebalancing your portfolio. Unlike stocks or bonds, it’s a type of asset where value depends on nothing but a shared belief that the gold price will rise on a sustained basis.

The most essential thing is a proper asset allocation, both equity and gold mutual funds must be a part of your portfolio. For long term investment, equity mutual funds should form core of the portfolio with gold funds acting as a hedge to balance and add stability to the overall portfolio. So, invest in a gold fund once you have built a well-diversified portfolio of equity mutual funds with 5 to 10% portfolio allocation to gold.

Suresh Kumar Narula is founder and Principal Financial Planner at Prudent Financial Planners. He has earned the professional CERITIFIED FINANCIAL PLANNER and got registered with SEBI as Investment Advisor. He writes on personal and financial planning articles and got published in Dainik Bhaskar, Business Bhaskar and The Financial Planner’s Guild, India. He is also a member of Financial Planner’s Guild India ( An association of practicing SEBI registered Investment advisers) to create awareness about Financial Planning in general public, promote professional excellence and ensure high quality practice standards. Suresh received his an M.com from Himachal Pardesh University and an MFC from Punjab University, Chandigarh. He can be reached at info@prudentfp.in